Blog

The enterprise marketing stack has never been more fragmented. The average brand team in 2026 manages content production across 8 to 12 channels, coordinates creative output with 3 to 5 agency partners, and attempts to enforce brand consistency across dozens — sometimes hundreds — of distributed users. Meanwhile, the tools they use to do it were built for a different era.

DAMs were designed to store and retrieve. Design tools were designed for specialists. Creative services were designed for campaigns, not operations. None of them were designed for what enterprise marketing actually needs today: a system that learns a brand and scales that intelligence at the speed of content.

This is where the category of AI brand management platforms emerges — and where the buying decision gets genuinely complex.

A recent internal benchmark from Pupila shows that enterprise brands operating with traditional DAM + agency workflows spend, on average, 90% of their marketing budget on media — yet creative quality drives 49% of campaign results. The math is broken. And the tools that were supposed to fix it haven't kept up.

This guide exists to help CMOs and VP Marketing leaders evaluate the platform landscape with the criteria that actually matter. Not feature checklists. A decision framework.

Before evaluating vendors, it's worth establishing a clear definition — because the market is using the term loosely, and conflating different categories leads to expensive mistakes.

An AI brand management platform is a system that centralizes brand intelligence (visual identity, tone of voice, persona definitions, photographic style, key messaging) and uses that intelligence to generate, govern, and distribute on-brand content at scale — across users, channels, and markets.

This is distinct from three adjacent categories that often appear in the same RFP:

Digital Asset Management (DAM) tools like Bynder and Frontify organize and retrieve assets. They solve the "where is the file" problem. They do not solve the "create a new on-brand asset in 3 minutes" problem. AI has been added to many DAMs as a bolt-on layer — search improvements, metadata tagging, basic recommendations — but the generation and governance intelligence is not native.

Design tools like Canva Enterprise democratize layout production. They are powerful for teams that need templates and visual flexibility. They do not learn a brand over time, do not enforce brand rules at the generation layer, and do not integrate with performance feedback loops that improve creative output.

Creative services and AI content tools like Jasper, Writer, or Typeface generate content at speed. Jasper and Writer are text-focused. Typeface is the closest AI-native competitor in the enterprise space — founded by Adobe's former CTO, valued at $1B in 2023, serving Fortune 500 clients — but it concentrates on American enterprise and lacks the regional relevance layer (cultural adaptation, local representation, market-specific personalization) that global brands increasingly require.

The gap that the AI brand management category fills is the intersection of all three: brand intelligence that is native, creation that is generative, and governance that is automated.

The competitive map has four distinct tiers. Understanding them clarifies positioning and purchase decision logic.

Bynder (Netherlands, 2013) and Frontify (Switzerland, 2013) are the incumbents. Both were built as enterprise DAM and brand guidelines platforms, and both have added AI capabilities as extensions rather than foundations.

Bynder serves 4,000+ brands from SMB to Fortune 500 after an aggressive mid-market expansion. Pricing starts at approximately $450/month. Its AI is focused on DAM enhancement: search, auto-tagging, smart recommendations. Creating net-new generative assets is not its core function.

Frontify built its reputation around brand guidelines and templates. It serves enterprise clients including Uber, Microsoft, and Volkswagen. Pricing starts at $29/user/month. The platform is excellent at structuring and distributing brand rules — but brand rules are not brand generation. Frontify organizes; it does not create.

What they get right: Governance, user permissions, enterprise SSO, integrations with existing design stacks.

What they miss: Generative creation from brand intelligence, regional visual adaptation, performance feedback loops that make the platform smarter over time.

Typeface is the most serious AI-native competitor in this buyer conversation. Enterprise-first, expensive (custom pricing, often six to seven figures annually for enterprise deployment), and purpose-built for large marketing organizations. If your organization is a Fortune 500 with a US-centric creative operation and a significant budget for AI tooling, Typeface warrants serious evaluation.

Jasper and Writer are strong in text-led workflows. If your primary challenge is copy production at scale — blog posts, email, ad copy, product descriptions — these tools are mature and well-integrated. They are not, however, multimodal brand platforms. They do not handle visual brand intelligence.

Adobe GenStudio represents the incumbent's response to AI-native disruption. It carries Adobe's formidable ecosystem and enterprise relationships, but also its complexity, its procurement process, and its pricing architecture. For organizations already deep in the Adobe Creative Cloud stack, it deserves a look. For organizations evaluating fresh, it may be overbuilt for the actual problem.

Papirfly (Norway) dominates in European enterprise with a template-and-DAM approach that emphasizes brand governance. Strong in regulated industries. Limited in generative capability. Templates control output, but they also constrain creativity.

Canva Enterprise occupies the democratization layer — it has scale (used by the majority of enterprise marketing teams in some capacity) but not depth. Brand intelligence in Canva is shallow by design; the platform's value proposition is accessibility, not governance.

This tier is where Pupila sits — and it is currently the smallest tier by number of players, which is precisely why it represents a category-defining opportunity for buyers who want to establish a competitive creative advantage before this approach becomes standard.

A brand-native AI platform is architecturally different from the platforms above. The AI is not a layer added to an existing product; the AI is the product. The intelligence the platform builds about your brand — visual identity, tone, personas, photography style, key messages — directly drives every generation, every governance rule, and every performance insight.

The following framework maps to the actual purchasing questions that enterprise marketing leaders face when evaluating this category. Use it as a decision scaffold, not a scoring rubric.

This is the foundational question. Most platforms in this category — including incumbents — treat brand guidelines as a reference library: assets are uploaded, rules are documented, templates are built. Users consult the guidelines. Compliance is manual.

A brand-native AI platform inverts this architecture. The brand identity becomes a model — a set of learned parameters that actively shapes every generation. Ask vendors: what happens when a user generates an image with no explicit style prompt? Does the output default to generic AI aesthetics, or does it default to your brand?

The Banco do Brasil deployment illustrates the operational implication of this distinction. With five active sub-brands (BB Varejo, BB Corporate, BB Estilo, BB Private, BB Empresas) and 213 active users — including 10 partner agencies — the central brand team cannot manually review every asset. Brand compliance has to happen at the generation layer, not the approval layer. In one year of operation, the platform generated 53,254 images, 1,152 videos, and 8,558 brand variations, with a peak of 900+ assets per day in September 2025. The Creative Director, Cláudio, noted that "Pupila became a great ally for both our internal teams and partner agencies" precisely because compliance was built in, not bolted on.

Key evaluation questions:

Enterprise brand management requires multimodal output: photography-style images for campaigns, video for social, copy for multiple channels, and the ability to adapt all of the above for different markets, segments, and moments.

Evaluate platforms on their native generative capabilities — not on integrations with third-party generation tools that introduce consistency gaps. The value of a brand-native platform is that generation happens inside the intelligence layer. When image generation is outsourced to Midjourney or DALL·E via integration, the brand intelligence cannot fully constrain the output.

Wellhub's deployment demonstrates the personalization dimension of generative capability. The platform enables content generation along three distinct axes simultaneously: by age segment (20s, 35, 50+), by interest (tennis, crossfit, yoga), and by city (São Paulo, Los Angeles, Milan). This is not template-based customization — it is generative personalization at a scale that agencies cannot match economically.

Key evaluation questions:

The enterprise scaling challenge is not a technology problem — it is a governance problem. Large organizations need to extend creative capability to non-designers, regional teams, partner agencies, and local market operators. Every extension of the user base is a potential inconsistency vector.

The critical metric here is not "how many users can the platform support" (all enterprise platforms can support large user counts) but "what percentage of users are generating on-brand content without specialist oversight."

In the Avenue deployment, the fintech's rebranding challenge was precisely this: how do you maintain visual consistency for a new brand identity when stock photography no longer matches the brand and full photo shoots are economically prohibitive? With 135 active users distributed across the organization, manual review was not a viable oversight mechanism. As Avenue's Ricardo noted: "When tools are fragmented, creation data is fragmented — which reduces control, increases management complexity, and can compromise the governance of what is being produced." A unified platform resolved the governance issue structurally.

Key evaluation questions:

This criterion separates platforms that are purely production tools from platforms that are strategic assets. A brand management platform that integrates performance data — which creative variations drive engagement, which visual styles correlate with conversion, which messaging angles outperform benchmarks — creates a feedback loop that makes the brand smarter over time.

The business case here is supported by an important data point: research by Viget Agency and NCSolutions demonstrates that high-quality creative drives 4.7X the ROI of average creative. Yet the typical enterprise marketing budget allocates 90% to media and 10% to creative production. A platform that continuously improves creative quality through performance feedback compresses this ROI gap every month it is in use.

Key evaluation questions:

Enterprise brand management has hidden costs that standard vendor pricing does not capture. Agency dependency is the largest: the cost of briefing, producing, revising, and approving assets through external creative partners — for what are often recurring, operational demands — represents a significant budget line that a brand management platform should substantially reduce.

Badia Spices provides a reference point. The company operates across 80 countries with a marketing team of four people. Per their CEO Scott Moffitt: "Work that would take months and cost thousands was made viable in much less time." The platform delivered a 41.8% improvement in ROAS. The relevant frame here is not the platform's annual cost — it is the cost of the alternative.

When comparing platforms on TCO, account for: licensing cost, implementation and onboarding investment, ongoing agency dependency reduction, internal headcount efficiency, and the value of consistency (every inconsistent asset is a brand dilution event with compounding effects on recall and trust).

Key evaluation questions:

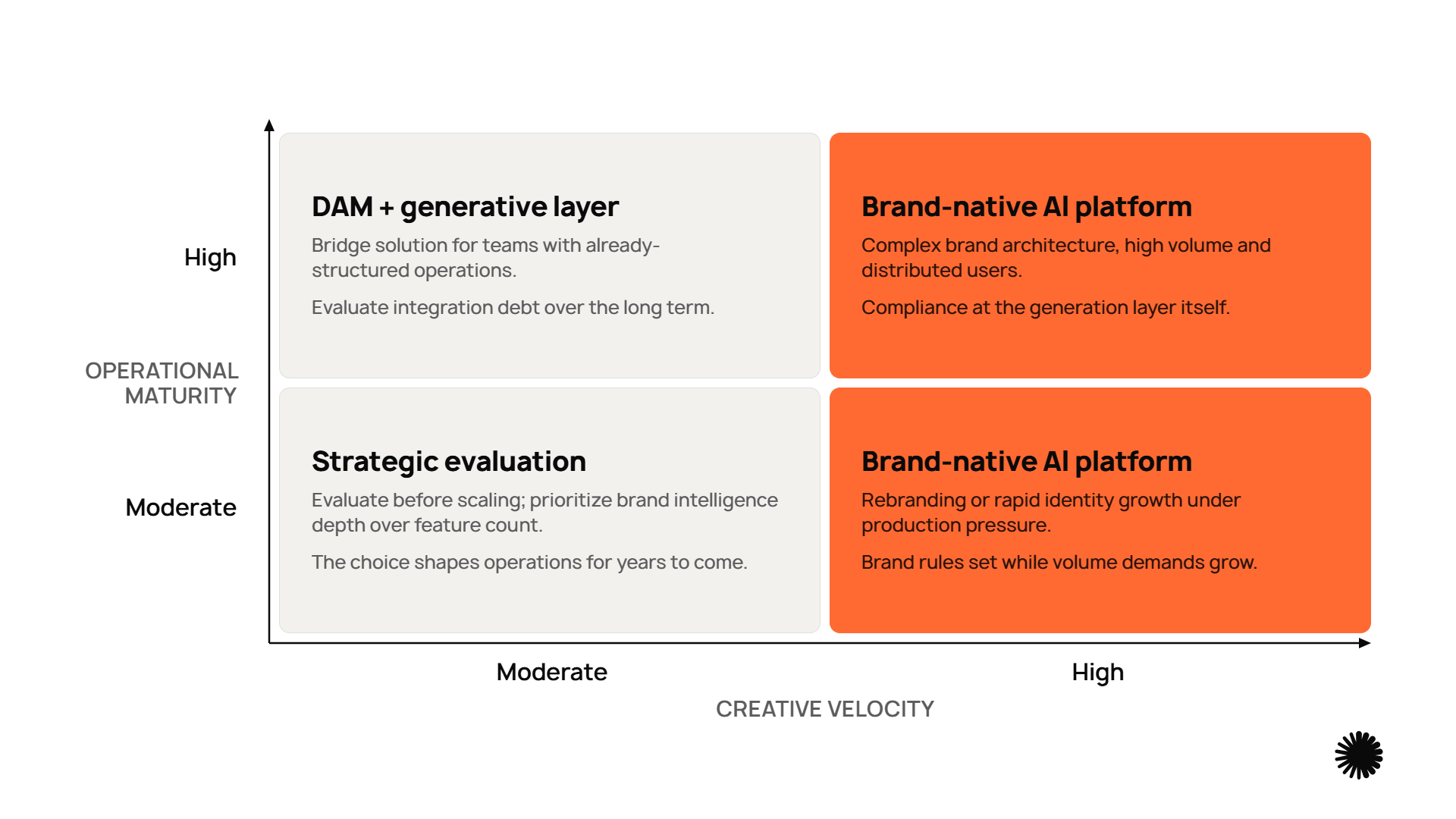

Use the following framework to position your organization's evaluation. It maps two dimensions: your current operational maturity (how structured your current brand management is) and your creative velocity need (how much content volume you need to produce)

High operational maturity + high creative velocity: You need a brand-native AI platform with deep brand intelligence and generative capability at scale. This is the Banco do Brasil scenario — complex brand architecture, high volume, distributed users. Pupila and Typeface are both serious options; the differentiator is whether regional relevance and performance integration matter for your operation.

High operational maturity + moderate creative velocity: Your current DAM may be working, but you are missing the generative layer. Frontify or Bynder with a generative add-on may be a pragmatic bridge. Evaluate whether the bolt-on approach will create integration debt over a 3-year horizon.

Moderate operational maturity + high creative velocity: This is a rebranding or rapid-growth scenario — like Avenue. Brand rules are being established or revised while production demands are increasing. A brand-native AI platform built for exactly this transition will deliver faster ROI than a DAM that requires brand guidelines to be fully mature before generating value.

Moderate operational maturity + moderate creative velocity: You are evaluating a platform ahead of scaling. Invest the evaluation time now; the platform you select will shape your creative operations for the next 3 to 5 years. Prioritize brand intelligence depth over feature count.

Before requesting a demo or entering a procurement process, use these questions to qualify vendors at the conversation stage:

On brand intelligence: "If I give you our brand guidelines today, what happens to them technically? How do they influence generation six months from now?"

On regional relevance: "We operate in [N] markets. How does the platform adapt visual output for cultural context, demographic representation, and local market norms?"

On governance: "We have [N] users, including external agencies. How does your permission architecture work, and what happens when a user tries to generate something off-brand?"

On performance: "How does the platform connect creative output to performance data? Show me what that feedback loop looks like in the product."

On TCO: "Can you model the ROI for an organization with our profile? What assumptions drive it, and what reference clients can I speak with?"

On roadmap: "Where is AI model improvement on your roadmap? How do I know the platform I buy today will be meaningfully better in 18 months?"

Pupila is a Brand Experience Platform built on the premise that brand intelligence should be the foundation of every creative decision, not a reference document sitting outside the tools where work happens.

The platform integrates three layers that the competitive landscape has not yet combined in a single product:

Brand Intelligence Hub — The layer that learns, centralizes, and continuously refines everything that defines the brand: visual identity, tone of voice, personas, photographic style, key messages, competitive positioning. The more the platform knows, the more precise every generation becomes. This is not a static brand guidelines upload; it is a living model that improves with every interaction and every performance signal.

Brand Studio — The generative creation layer. Image, video, copy — all generated from the brand intelligence model rather than from generic AI models. The difference is measurable: outputs are on-brand by default, not by correction. This is the layer that enables the Banco do Brasil scenario (213 users, 900+ assets/day, consistent across 5 sub-brands) and the Badia Spices scenario (4-person team, 80 countries, +41.8% ROAS).

Marketing Powerhouse — The distribution and performance layer. Assets flow from creation to channel, performance data flows back from channel to the brand model. The platform gets smarter about what works for your brand over time.

Pupila's current client base spans 25+ enterprise brands across financial services, technology, fitness, food and beverage, and education — including Banco do Brasil, Avenue, Wellhub, Mercado Livre, Creditas, and Badia Spices. The platform is deployed in Brazil, the United States, and global operations from those clients.

Pricing is structured by brand complexity and team scale, not per-seat — a deliberate design choice that removes the disincentive to expand adoption across the organization.

The enterprise buyer evaluating AI brand management platforms in 2026 is navigating a market in transition. DAMs built for storage are adding AI. AI tools built for content production are being positioned as brand management. The marketing from every vendor in this space will sound similar. The underlying architecture is not.

The question that clarifies the evaluation is simple: does the platform learn your brand, or does your brand have to conform to the platform?

Tools that require your team to start from templates, choose from style presets, or manually enforce brand rules on AI-generated outputs are asking your brand to conform to their system. Platforms where brand intelligence is the model — where every generation, every governance decision, and every performance insight flows from a deep, continuously updated understanding of your brand — learn your brand.

For enterprise organizations where brand consistency at scale is a strategic asset, not just a compliance requirement, that distinction drives the investment decision.

Ready to evaluate Pupila for your organization? → Request a demo

Pupila is a Brand Experience Platform and the defining product in the AI Brand Management category. Clients include Banco do Brasil, Avenue, Wellhub, Badia Spices, Mercado Livre, and 25+ enterprise brands across 5 continents.

Related reading:

<

>

All rights reserved @ 2024

All rights reserved @ 2024